In his address on February 16th, Deputy Prime Minister and Minister for Finance, Mr. Lawrence Wong, unveiled the Singapore Budget Statement for the Financial Year 2024, providing crucial insights for businesses.

Acknowledging the challenges of the preceding year marked by global economic uncertainty, Minister Wong emphasized Singapore’s resilience amid subdued global growth, with the economy expanding by a modest 1.1%. Against this backdrop, the budget outlined strategic measures aimed at bolstering businesses and fostering economic growth within Singapore.

The measures impacting companies have been split into 2 categories, below is a clear and simple recap to be able to understands their impacts on businesses.

In this article, we will cover:

- Introduction

- Enterprise Disbursements

- Tax Changes

- Extension of the SkillsFuture Enterprise Credit

- Enhancements to the Enterprise Financing Scheme

- Conclusion

Enterprise disbursements and tax changes

Enterprise disbursement

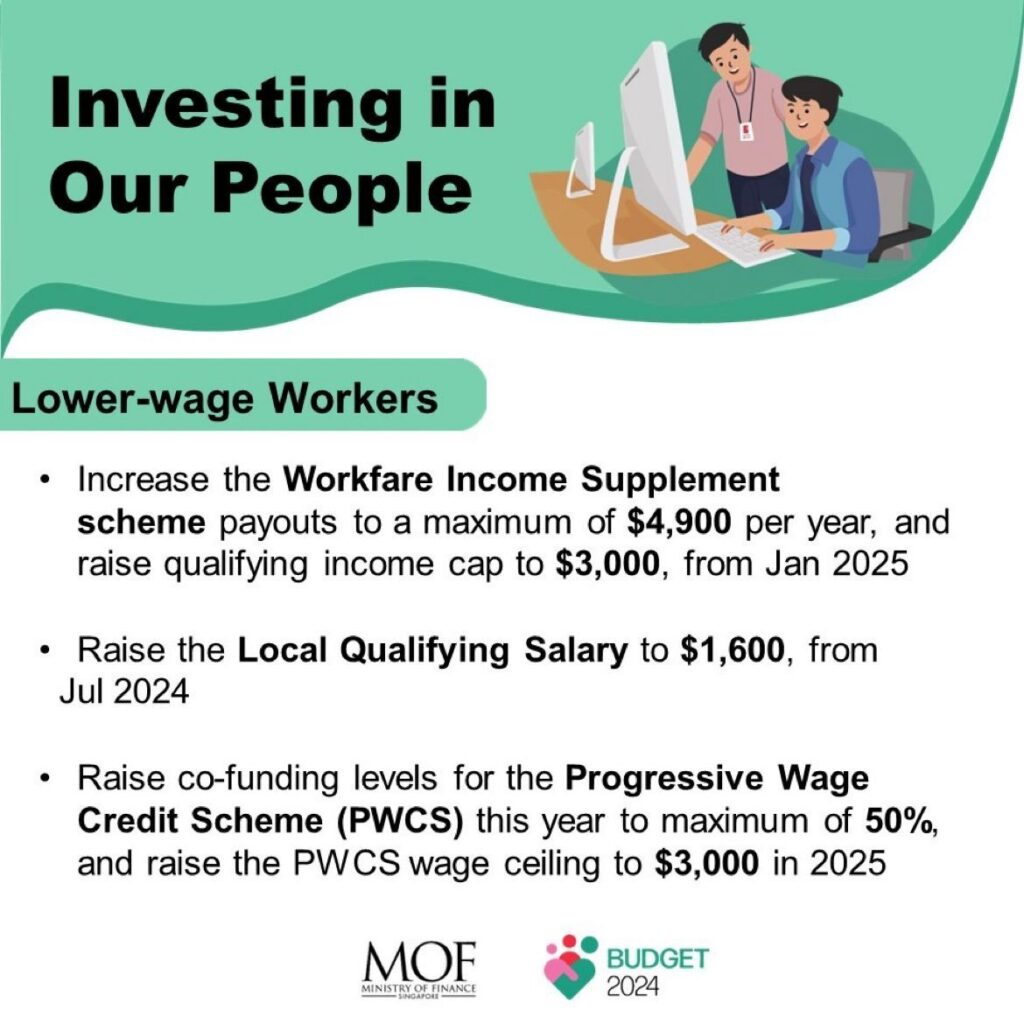

There will be enhancements to the Progressive Wage Credit Scheme (PWCS) to raise the PWCS co-funding levels and wage ceiling for PWCS co-funding support, as well as introduce a wage cut-off for PWCS eligibility.

The PWCS was introduced for the first time in 2022 and supports employers by co-funding wage increases for lower-wage workers. In 2024 budget:

1. PWCS co-funding support will be raised for wage increases given in the qualifying year 2024 from 30% to 50% for employees with gross monthly wages of up to $2,500, and 15% to 30% for employees with gross monthly wages more than $2,500 and up to $3,000.

2. The gross monthly wage ceiling for PWCS co-funding will be increased from $2,500 to $3,000 in qualifying years 2025 and 2026.

3. From 2024 onwards, PWCS support will not be applicable to employees whose average monthly wage exceeds $4,000 post-wage increase.

Tax changes

The Singapore Budget 2024 introduced 12 new tax measures for Businesses, here’s a recap of the most relevant ones and how will impact companies in Singapore:

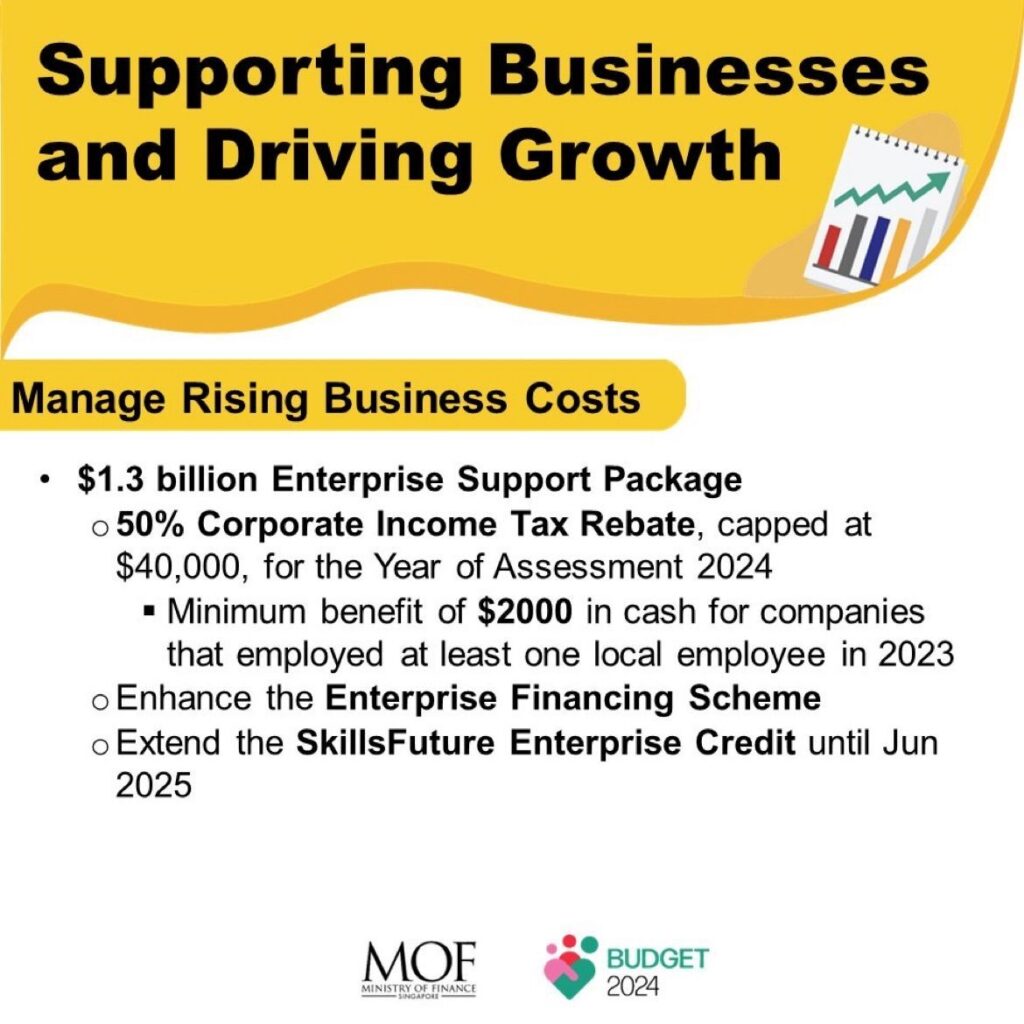

1. Corporate Income Tax (“CIT”) Rebate

To help companies manage rising costs, a CIT Rebate of 50% of tax payable will be granted for YA 2024, capped at S$40,000. Companies that have employed at least one local employee in 2023 will receive a minimum benefit of $2,000 in the form of a cash payout.

Companies that have met the local employee condition will automatically receive the CIT Rebate Cash Grant by 3Q 2024. The CIT Rebate will be automatically incorporated in companies’ tax assessments raised after they file their Form C-S/ Form C-S (Lite)/ Form C for YA 2024.

Implement the Income Inclusion Rule (“IIR”) and a Domestic Top-up Tax (“DTT”) under Pillar Two of the Base Erosion and Profit Shifting (“BEPS”) 2.0 initiative.

Singapore will implement the IIR and a DTT, which will impose a minimum effective tax rate of 15% on businesses’ profits from financial years starting on or after 1 January 2025. This will apply to relevant multinational enterprise (“MNE”) groups with annual group revenue of 750 million euros or more in at least two of the four preceding financial years (referred to as “in-scope MNE groups”), in line with the Pillar Two Global Anti-Base Erosion (“GloBE”) Model Rules.

The IIR will apply to in-scope MNE groups that are parented in Singapore, in respect of the profits of their group entities that are operating outside Singapore. The DTT will apply to in-scope MNE groups in respect of the profits of their group entities that are operating in Singapore.

2. Refundable Investment Credit (RIC)

The Refundable Investment Credit (RIC) incentivizes companies to undertake significant investments that contribute to substantive economic development in Singapore’s key sectors and emerging growth areas. Serving as a tax credit with a cash refund option, the RIC is designed to stimulate high-value economic endeavors. These may include the establishment or expansion of manufacturing facilities, investment in innovative research and development initiatives, and support for environmentally sustainable practices in line with the nation’s green transition objectives.

It will be awarded on an approval basis, through the Singapore Economic Development Board (EDB) and Enterprise Singapore (EnterpriseSG).

The RIC will support high-value and substantive economic activities such as:

a. Investing in new productive capacity (e.g., new manufacturing plant, production of low-carbon energy);

b. Expanding or establishing the scope of activities in digital services, professional services, and supply chain management;

c. Expanding or establishing headquarter activities, or Centres of Excellence;

d. Setting up or expansion of activities by commodity trading firms;

e. Carrying out R&D and innovation activities; and

f. Implementing solutions with decarbonisation objectives.

The RIC is awarded on qualifying expenditures incurred by the company in respect of a qualifying project, during the qualifying period. Each RIC award will have a qualifying period of up to 10 years.

The credits are to be offset against Corporate Income Tax payable. Any unutilised credits will be refunded to the company in cash within four years from when the company satisfies the conditions for receiving the credits.

3. Introduce an additional Concessionary Tax Rate (“CTR”) tier of 15% for the Intellectual Property Development Incentive (“IDI”)

An additional CTR tier of 15% will be introduced under the IDI with effect from 17 February 2024. IDI encourages companies that use and commercialize intellectual property rights (IPR) arising from R&D in Singapore.

Tax at a concessionary rate would be imposed on a percentage of your entity’s qualifying intellectual property (IP) income derived during the incentive period. Qualifying IP income refers to royalties or other income receivable by the approved IDI company as consideration for the commercial exploitation of qualifying IPR.

More Tax Measures have been introduced to support specific industries such as the wealth management industry, the aircraft industry, as well as the one of global trading.

Supporting businesses and driving growth

The Ministry of Finance has also introduced the extension and enhancement of two important schemes in support of businesses:

Extension of the SkillsFuture Enterprise Credit (“SFEC”)

The SFEC encourages employers to undertake enterprise and workforce transformation initiatives. Eligible firms have received a one-off credit of up to $10,000 to cover up to 90% of out-of-pocket expenses for supportable enterprise capability development and workforce transformation programs.

The SFEC will be extended for a year to 30 June 2025. This means that employers who have already received the SFEC will be able to use it on supportable schemes beyond 30 June 2024, with claims to be submitted by 30 June 2025.

Enhancements to the Enterprise Financing Scheme (“EFS”)

The Enterprise Financing Scheme (EFS) has been instrumental in facilitating easier access to financing for Singaporean enterprises across various stages of growth. As part of the Enterprise Support Package, three significant enhancements are set to fortify the EFS framework.

1. The maximum loan quantum for the EFS – SME Working Capital Loan will be permanently elevated from $300,000 to $500,000. This enhancement aims to aid SMEs in addressing heightened working capital and operational cash flow requirements, particularly amidst rising costs.

2. The extended maximum loan quantum of $10 million under the EFS – Trade Loan will remain in effect until 31 March 2025. This extension is geared towards bolstering businesses’ internationalization endeavors, crucially supporting them amid disruptions in global supply chains.

3. The extension of support for domestic construction projects through the EFS – Project Loan until 31 March 2025, with a maximum loan quantum of $15 million, seeks to provide essential backing to domestic construction firms navigating a challenging operating landscape.

These enhancements underscore the government’s commitment to fostering a conducive environment for business growth and resilience in Singapore.

In conclusion, the Singapore Budget 2024 brings forth a comprehensive set of measures aimed at supporting businesses in navigating the challenges of an uncertain global economic landscape. Through enhancements to schemes like the Progressive Wage Credit Scheme and various tax incentives, the government seeks to bolster productivity, encourage investment, and foster innovation across different sectors. Overall, the Budget 2024 reinforces Singapore’s pro-business environment and underscores its commitment to fostering sustainable growth and development in the years to come.